Sorting For Circularity Europe: An Evaluation And Commercial Assessment Of Textile Waste Across Europe

Executive Summary

Fibre-to-fibre textile recycling commitments and policies are continuously increasing, as one of the key strategic components propelling organisations to support the transition towards a circular fashion industry. In turn, these developments are expected to drive an increased demand for post-consumer textiles collection, sorting and recycling infrastructure across the EU. Scaling this infrastructure will require substantial investment. In order to holistically inform any future investments, there is a need to understand both the characteristics of post-consumer textiles available in the European market as well as the business case for monetisation through recycling. The Sorting for Circularity Europe Project was created to address this knowledge gap, exploring these materials in depth. The Project is aimed at analysing types of waste being generated, quantities available as feedstock for recycling, and the ability to channel textile waste as feedstock for those with innovative solutions. This report is key as it is the first to provide powerful information on which informed decisions can be made for further investment, policy developments and next steps towards circularity.

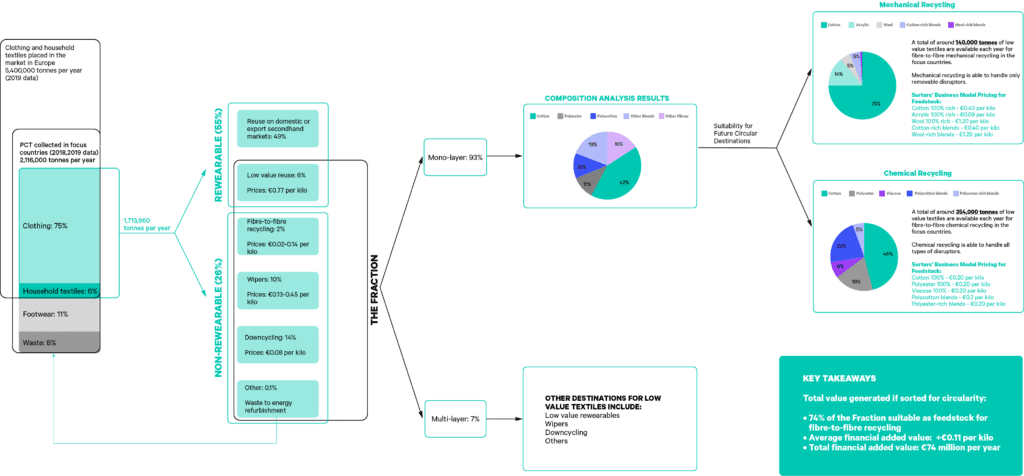

Overall, the Sorting for Circularity Europe study finds that a total of 494,000 tonnes each year —or 74% of low value post-consumer textiles, is readily available and suitable for closing the loop in the clothing and textiles sector across six European countries. These findings culminate in promising opportunities for recapturing value via mechanical and chemical recycling and resultantly diverting textiles away from less circular destinations like downcycling to non-wovens, insulation or filling material, the wipes industry and incineration. This represents a potential value increase of €74 million per year when sorted textiles are reintroduced into the textiles value chain.

The Sorting for Circularity Europe project aims to increase harmonisation between the sorting and recycling industry and stimulate a recycling market for unwanted textiles that can generate new revenue streams for sorters and unlock demand for recyclers and brands. Conducting analyses across Europe, in Belgium, Germany, the Netherlands, Poland, Spain, and the United Kingdom, the project provides the most comprehensive and representative snapshot of post-consumer textiles composition generated in Europe to date.

Sorting for Circularity is a framework conceived by Fashion for Good together with Circle Economy, with the aim to (re)capture textile waste, expedite the implementation of game changing technologies and drive circularity within the fashion value chain. The framework is based on insights from the Fashion for Good and Aii collaborative report “Unlocking the Trillion Dollar Fashion Decarbonisation Opportunity”, which charts a trajectory for the industry to meet its net-zero ambition by 2050, highlighting the potential and significant impact on carbon emissions in the industry through material efficiency, extended and re- use of waste. Created with scalability in mind, the project was first initiated in Europe, and has expanded to include Sorting for Circularity India.

LEAPING FORWARD THROUGH TECHNOLOGY

Using innovative Near Infrared (NIR) technology to determine garment composition, traditionally a task performed manually, the project analysed a total of 21 tonnes of post-consumer garments. On-the-ground examinations were performed over two time periods, autumn/winter 2021 and spring/summer 2022, to account for seasonal changes in the types of garments entering sorting facilities. The project focuses on textiles that cannot be reused in their original form (considered ‘non-rewearable’) and textiles that can only be resold at low prices (‘low value rewearable’). For readability purposes, these two categories are referred to as ‘the Fraction’ solely.

Cotton was found to be the dominant fibre (42%), albeit elastane might be present in a relevant share of this category. Cotton is followed by a large presence of material blends (32%), almost half of which consisted of polycottons (12%). Based on three characteristics, material composition, presence of disruptors, such as zippers and buttons, and colour, 21% of the materials analysed are deemed suitable as feedstock for mechanical recycling, while 53% are suitable for chemical recycling. However, it needs to be technically and financially viable to remove disruptors for chemical recyclers, otherwise only around one fifth of the total potential feedstock for chemical fibre-to-fibre recycling would be available.

Figure 1 presents an overview of the flow of clothing and household textiles from the moment they are placed on the market, to the volumes being collected in the focus countries of this project, to their eventual destinations. For the Fraction there is an indication of the breakdown by fibre composition and colour where relevant. The potential recyclability of these textiles is shown through the possible use cases for the different fibres, either for mechanical or chemical recycling and its related potential prices per kilo of material.

FIGURE 1: FLOW OF END-OF-USE TEXTILES FROM MARKET PLACEMENT TO FINAL DESTINATIONS. SOURCE: CIRCLE ECONOMY AND FASHION FOR GOOD (2022)

BUILDING A ROBUST SORTING AND RECYCLING INFRASTRUCTURE

In addition to this report, two further industry resources are available; Recycler’s Database, a database mapping textile recycler’s capabilities, illuminating crucial gaps between the sorting and recycling industry, and an open source Sorters Handbook to guide and support the sorting industry should they wish to do new or further analyses. Building off the project, two open digital platforms, Reverse Resources and Refashion Recycle, have been identified as critical tools to further enable the connections needed to match textile waste from sorters with recyclers, driving greater circularity in the years to come. Following an assessment of suitable digital platforms within and outside of the textile industry, Reverse Resources have 39 active recyclers and 32 active waste handlers/sorters on their platform, while Refashion Recycle have 103 recyclers and 66 sorters onboarded onto their platform. This represents a large portion of the European circularity industry.

PATH TOWARDS A CIRCULAR INDUSTRY

The amount of low value textiles collected is likely to increase, due partly to growing consumption and disposal, as well as driven by incoming legislation, for instance the Waste Framework Directive, that mandates the separate collection of textiles across Europe by 2025. However, the current and future potential of these textiles for circularity is complex to capitalise on; feedstock prices for current destinations (e.g. wipers) are at times more economically viable than those offered for fibre-to-fibre recycling. This might change as current recycling technologies are scaled and further investment is made to integrate operations related to automated sorting and removal of disruptors into the sorting process.

Overall, a sound business case for sorting low value textiles is required in order to retain and increase sorting capacity in Europe. This further highlights the need for increased investment into infrastructure that can sort and prepare textiles for reuse and recycling. To support the retention and further development of this sorting capacity in Europe, policy and upcoming legislation will play a key role in ensuring the environmental, social and financial sustainability of these stages of the clothing and textiles value chain. Policy Hub, together with textile industry players, published a position paper in August 2022 outlining key recommendations for policy development that supports the advancement of textile waste circularity. The position paper can be read in full here.

The outcomes of this project point towards the following recommendations for the wider industry to enact:

For collectors, sorters, and recyclers –

- Use the Sorters Handbook and the Sorting for Circularity Europe report as a guide to conduct further trials and continue to build a knowledge of fibre composition, sorting and recycling processes. This could be further supported by local governments, industry and civil society engaging with textile or household waste streams.

- Provide open-access to trials and data that can support and direct investment into necessary infrastructure.

- Update and utilise the Recycler’s Database to build knowledge about mechanical and chemical recycling destinations.

- Join digital platforms such as Reverse Resources and Refashion Recycle to unlock and connect supply with demand for post-consumer textiles.

For brands and manufacturers – 74% of the low value post-consumer textiles could be used as feedstock for recycling. Whilst this is a considerable share, this still leaves 26% without a circular destination due to their composition, the presence of multiple layers and/or non-removable disruptors.

- Prioritise designing for appropriate lifecycles. Hence, products that are designed for longevity should have a strong focus on durability and longevity. Ultimately, recycling should be a last resort for textiles, in accordance with the waste hierarchy, and not a goal in itself.

- Further commit to adopting circular design practices prioritising mono materiality, reducing disruptors where possible and incorporating recycled fibres into product portfolios as mandated by the Ecodesign for Sustainable Products Regulation in the European Union.

For policymakers – Sorting activities in European countries are at risk of being unable to continue their business as usual if the share of these lower value textiles in volumes collected continues to increase. Additionally, current sorting and logistics costs may pose a financial challenge for chemical recyclers to purchase these sorted textiles at scale. Therefore, it is important that policymakers, where required, utilise report findings to inform policy consultations and regulations.

For consumers – take into account that the purchase and disposal choices you make also have an influence on the end of use of these textiles. As far as possible, try to prioritise purchases of mono material products, or blends limited to two compositions, limited aesthetic trims and accessories. As a citizen, follow the instructions from your municipality to correctly dispose of your clothing and home textiles. Try repairing, reselling and swapping as activities to extend the lifetime of your products.

This report outlines the results from Phase 1 of the Project, which includes a comprehensive composition analysis of low value textiles using NIR technology to understand what and how much potential feedstock for fibre-to-fibre recycling is generated across European countries. The report also discusses future business models required for sorters to commercialise low value textiles and reflects upon the upcoming policy landscape in the European Union. Phase 2 of the report looks at understanding and supporting digital platforms that match supply and demand by connecting sorters and recyclers through waste mapping and match-making capabilities. Lastly, the report concludes with recommendations for various stakeholders to progress necessary action in the sorting and recycling industries.